“The business continues to hit on all cylinders,” said Uber’s CEO yesterday. The stock declined.

Palantir beat expectations, raised guidance, what we call in the industry a “beat and raise.” The stock fell about 8%.

Demand, our 10-point sentiment algorithm metering buying and selling, peaked on Halloween at 5.9 and is declining. But Supply (our proprietary treatment of Reg SHO Short Volume) is below the 5, 20, 50 and 200-day reads.

It’s “new month, new money,” when money flowing to systematic retirement accounts gets deployed. Yet broad measures are now down about the same percentage since Oct 29 that they fell in a day Oct 10.

And it’s earnings season.

Set all that aside.

In a way the biggest number of the day is a three-digit one: 100. That’s the DXY, index of the US dollar versus a global basket. For the first time since May, it’s over 100. A sharp rise in the dollar can hit risk assets like equities that tend to inversely correlate.

Our money loses value every year because the supply of it outstrips output. Ron Baron, Baron Funds, says he trades depreciating assets called dollars for appreciating assets called stocks.

If the appreciation outpaces the depreciation, we make money. If not, we don’t. It’s a weird, once-in-history construct. Never until this modern era have global governments coordinated the destruction of their currencies as policy for prosperity.

I paid $18 for two large coffees Monday at the Phoenician (built lavishly by Charles Keating for you oldsters like me who might remember him) in Scottsdale before flying back to the Centennial airport via JSX. That’s a good way to travel by the way. You cut out big airports as middlemen. Scottsdale to Centennial.

We took quite a few Ubers there too, and it seems the typical vehicle is a black Chevy Suburban, black GMC Denali, etc. And every Uber ride is more than a taxi now. Yes, you get to pick what you want – Black, Comfort, Pet, etc. By phone in the palm of your hand. But still. Uber started by cutting the cost of transportation.

And Nov 3, stocks traded with different round lots. I’ve said that the thing that will crack this market is technology, the engine. Not tech stocks but something awry with technology. Because it’s a data network.

Stocks under $250 continue to quote in round lots of 100 shares. Doesn’t mean they trade there. Stocks over $250-$1,000 quote in 40-share increments. There to $10,000, 10 shares. Over $10,000, one share. You can easily track these group with our decision-support platform, Market Structure EDGE, investors.

Just BRK.A now has a round lot of a single share. Watch the volume in that stock. Will there now be statistical arbitrage in Berkshire Hathaway for the first time? Don’t know.

On Nov 3, there were 19 stocks priced between $1,000-$10,000, with NVR the highest priced, near $7,100. There were 184 stocks $250-$1,000.

But FDX straddling $250 COULD conceivably have a bid for 100 shares, and an offer of 40, with the bid and offer straddling the line. Is that a problem? Maybe. We’ve never before had a regulatory requirement to post the best bid or offer at different sizes.

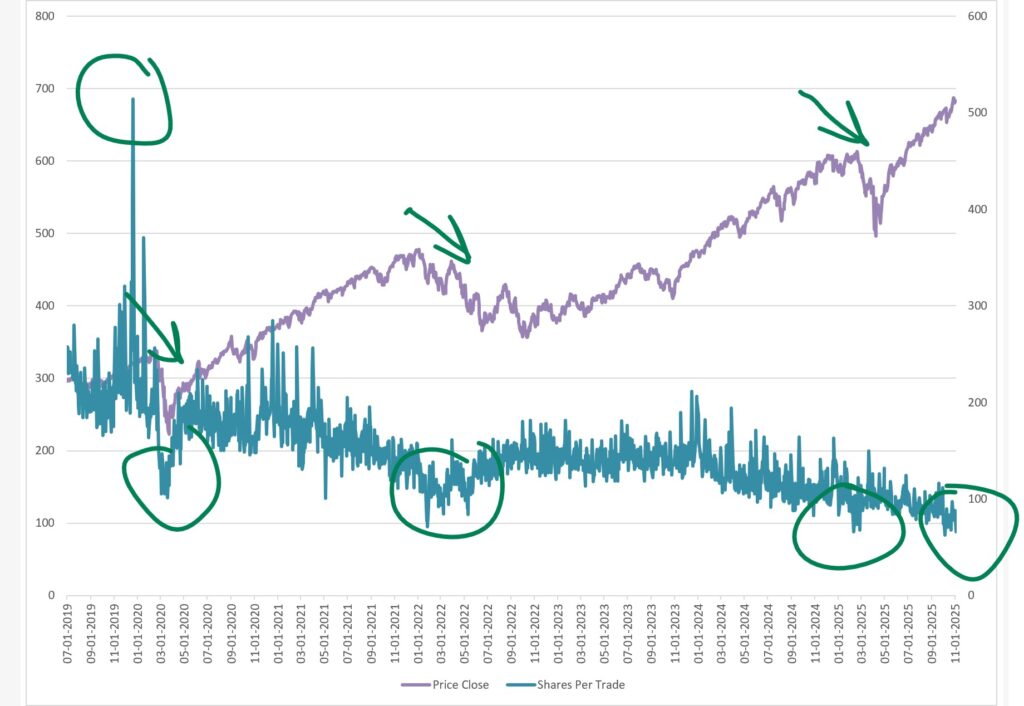

But trade-size has again plunged like it did in February this year.

This image I’ve inserted is SPY Jul 2019 to present. On Nov 3, the average trade-size was 66 shares. So far as I can tell, the all-time low was 62 shares Oct 6 (before the Oct 10 plunge).

Trade-size dropped in the Pandemic correction, leading into the 2022 correction. Before 2020, trade-size could jump north of 500 shares as it did during December 2019 quarterly index-rebalances. It doesn’t spike anymore with rebalances. Machines run everything.

Therefore, you look at machine data to understand what might go wrong. Rather like an automobile mechanic runs diagnostics to see what’s wrong with an engine. Auto mechanics don’t read economics reports or study quarterly earnings to understand what’s wrong with your car.

Just saying.

I think trade-size drops when machines setting prices can’t calculate outcomes and thus cut risk by speeding up the rate of change – resulting in smaller trades.

And because a great deal of those tiny trades are for keeping ETFs tracking some basket of stocks and related options, liquid and illiquid things can suddenly move differently.

That’s a bottleneck. Things can come apart at the seams (doesn’t mean they will).

If we want to know if or when something is good, humming, running like a top, check the data. And when we think something is knocking in the engine, we check the data.

You might think I’m always looking for knocks. Not so. There’s something wrong with the engine. Not my opinion. Look at trade-size. Doesn’t mean it can’t give us another 100,000 miles. But these data right now are the same as they were at each of the last big market-declines.

Public companies, you’re counting on this market to give you a barometer on your value. Don’t leave that to chance. Arm yourselves with data and a plan. We have both.